Keywords: credit card processing, merchant account, payment gateway, interchange fees, PCI compliance, chargeback protection, high risk merchant account, interchange-plus pricing, effective rate calculator, merchant services provider

If you accept online payments, you’ve probably asked: “Why are my credit card processing fees so high?” In 2025, costs are shaped by your merchant account, the payment gateway you use, network interchange fees, and your provider’s markup. In this guide, we unpack every component and show practical steps to reduce your effective rate—without risking compliance or cash flow.

Merchant account: a special bank account that lets you accept card transactions and receive settlements. Your “merchant services provider” underwrites risk, sets your pricing model (e.g., interchange-plus, flat rate, or tiered), and manages settlement, statements, and support.

(adsbygoogle = window.adsbygoogle || []).push({});

Payment gateway: the software layer that securely transfers card data between your checkout, the processor, and card networks. Gateways often add features like tokenization, 3-D Secure, fraud screening, and chargeback prevention. Some providers bundle the gateway and merchant account; others let you mix and match.

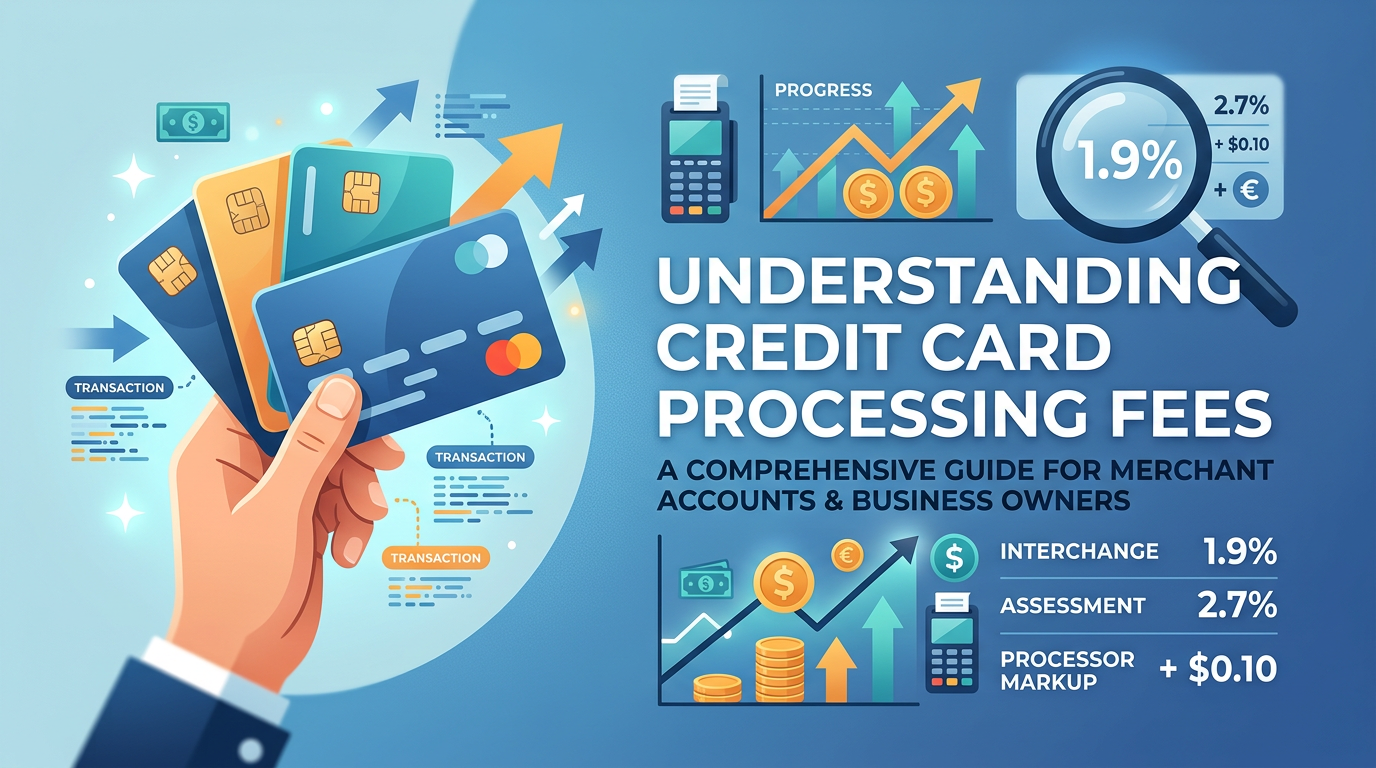

Interchange fees are set by the networks (Visa, Mastercard, etc.) and paid to the issuing bank. They vary based on card type (debit vs. rewards), transaction method (card-present vs. ecommerce), and risk signals. Assessments are small network fees added on top. You can’t negotiate interchange, but you can optimize to qualify for better categories (e.g., AVS, 3-D Secure, clean data, and accurate descriptors).

Your effective rate is total processing cost divided by total processed volume. It’s the single best metric to compare providers.

Effective Rate = (Total Fees ÷ Total Processed Volume) × 100

Target: Many healthy ecommerce stores can achieve an effective rate between 2.2%–2.7% with interchange-plus, clean data, and solid fraud controls. Your exact target depends on AOV, card mix, geographies, and risk profile.

PCI DSS protects cardholder data and reduces breach risk. Most ecommerce merchants fall under SAQ A or A-EP depending on how checkout is implemented. A good gateway will simplify PCI with hosted fields, tokenization, quarterly scans, and guided SAQs. While some providers charge a PCI compliance fee, staying compliant lowers your risk, improves approval rates, and avoids punitive charges.

Fraud hurts twice: you lose the sale and pay a chargeback fee. Keep your chargeback ratio below network thresholds with:

If you sell in a category with elevated disputes or regulatory scrutiny (supplements, digital subscriptions, tickets, etc.), you may be routed to a high-risk merchant account. Expect higher markups and rolling reserves, but you gain stability and fewer surprise shutdowns. Choose a provider that’s transparent on reserve terms, settlement schedule, and dispute management.

| Model | Pros | Cons | Best For |

|---|---|---|---|

| Interchange-Plus | Transparent, lower at scale, easy to audit | Statement looks complex | Growing ecommerce, B2B, subscription |

| Flat-Rate | Simple, predictable, easy to start | More expensive as volume/AOV grows | Startups, low volume, low AOV |

| Tiered | “Simple” on paper | Opaque, frequent downgrades, hard to compare | Generally avoid |

(adsbygoogle = window.adsbygoogle || []).push({});

With interchange-plus and clean data, many stores land between 2.2%–2.7%. High-risk categories or heavy rewards-card mixes will be higher.

Yes. PCI DSS applies to any merchant handling card data. Good gateways reduce your scope and provide scanning and SAQ support.

Use 3-D Secure on risky orders, keep descriptors clear, automate shipping notifications, and maintain flexible refund policies. Consider alerts or guarantee programs for peak seasons.

When your product category, dispute history, or business model triggers elevated risk. A specialized provider can keep you processing reliably—with clear reserve terms.

Move to interchange-plus, pass complete data, deploy chargeback protection, and audit your statements monthly. If you need help comparing quotes or setting up a compliant gateway, our US/UK team can assist.

Need a second opinion on your processing costs? Contact us for an effective rate review and best-fit merchant account recommendations.